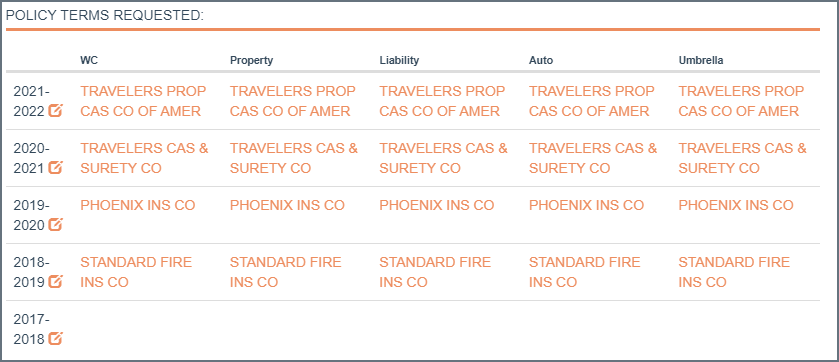

When it comes to managing the process, consider the scale. You may have 8, 12, 20 new business opportunities in the pipeline at a given time, each with one to seven lines of coverage and you’ll need three to five years of history. Make sure you have a conveyor belt set up. A template loss release form. The story is the same, only the names change (insured, carriers). A coverage matrix – policy terms down the column, Lines of Coverage across the top row (header).